CONTACTS: +254 726879488 (Mobile)

+254770 455 116 (Office)

Kenya’s Retirement Benefits Industry in Kenya has registered significant growth in its Assets Under Management (AUM) to Kshs 1.2 tn in June 2018, from Kshs 287.7 bn in 2008.

This growth has been driven by increased membership into various Retirement Benefits Schemes as a result of the Retirement Benefits Authority’s initiatives to increase pension penetration, currently at 15.0% of the adult population, by educating the public on the importance of saving for retirement, combined with increased contributions by members as the investing population continues to grow.

Part of this growth has also been attributed to the positive performance by Fund Managers, as investments returns are accrued to the schemes for the benefit of members. In this week’s focus note, we will analyze the 2018 performance by Fund Managers of Retirement Benefits Schemes, following reports released by Zamara (Formerly Alexander Forbes), and Actserve (Actuarial Services Company) on the 2018 returns declared by Fund Managers.

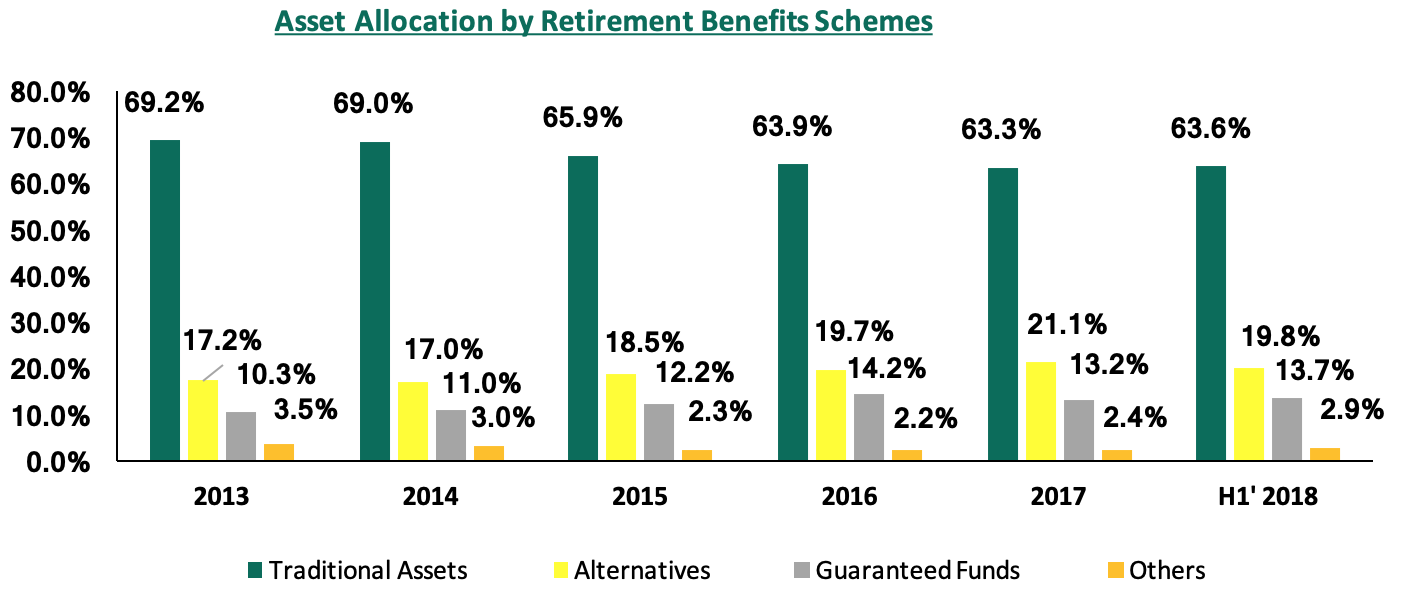

Changes in the Asset Allocation by Retirement Benefits Schemes in Kenya

Over the years, allocation by Retirement Benefits Schemes has been skewed towards traditional assets, which include Government Securities and Equities. The allocation to alternative assets, including Property, Private Equity, and REITs, has however been increasing, rising to 19.8% of total Assets Under Management (AUM) as of June 2018 from 17.2% in 2013. There is, however, room for improvement and growth as the regulations allow up to 70% allocation towards alternatives, i.e. (Property 30%, Private Equity 10%, REITs 30%).

Source: RBA Industry Report June 2018

Fund Managers’ low allocation in alternatives can be attributed to lack of expertise and experience with asset classes such as private equity and real estate, as investing in these asset classes requires detailed due diligence and evaluation as well as engaging legal, financial and sector-specific expertise.

Key Drivers that Determine the Investment Performance of Retirement Benefits Schemes:

Section II. Historical Performance by Retirement Benefits Schemes

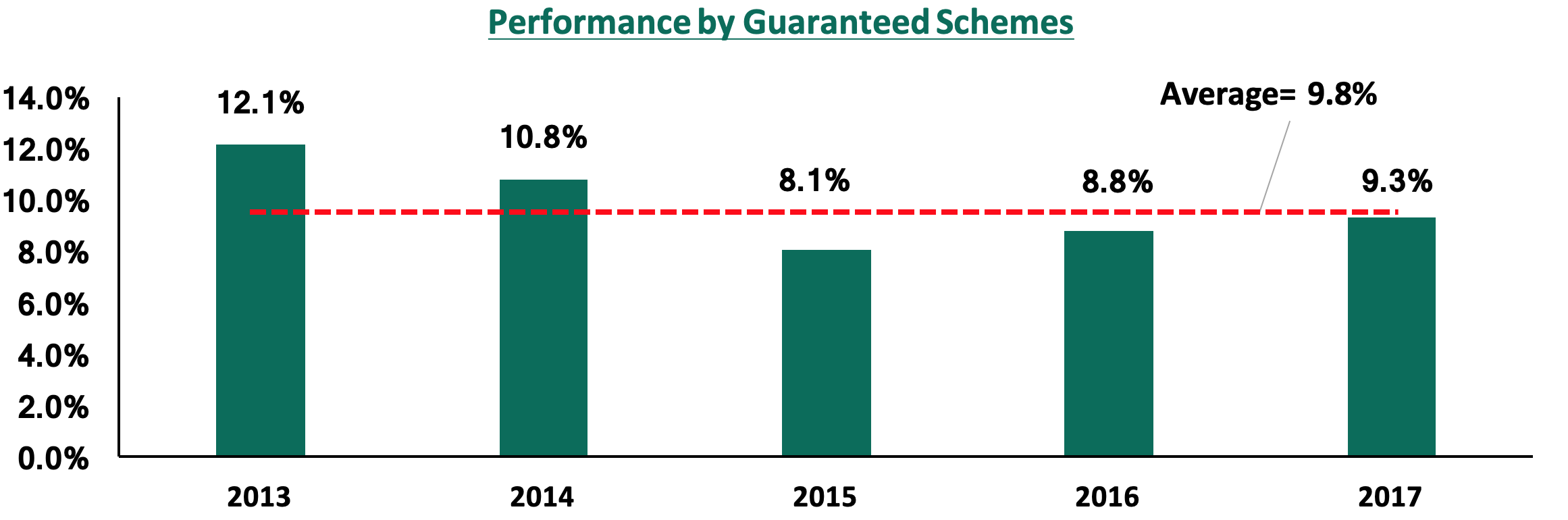

Guaranteed Schemes

Guaranteed Schemes are largely offered by insurance companies and they guarantee a minimum rate of return, with the maximum allowable rate that can be guaranteed is 4.0% p.a. The insurance companies, however, give higher returns based on the portfolio performance, as seen below:

Historically, guaranteed schemes have offered lower returns compared to segregated schemes, at a basic average of 9.8% in the last 5 years compared to the basic average of 11.3% for segregated schemes in the same period, as the insurance companies hold some reserve every year to cater for years where the performance of the market is below the promised rate. For instance, in the year 2013, guaranteed schemes declared a return of 12.1%, which was 8.0% points lower than the average return of 20.1% declared by segregated schemes.

However, in 2013 when markets dipped and segregated schemes declared an average return of 1.4%, guaranteed schemes declared a return of 8.1%, 6.7% points higher than the average return declared by segregated schemes. Guaranteed schemes are therefore attractive for members with a conservative risk appetite as the contributions are protected and a minimum return is guaranteed. The 2018 results for guaranteed schemes are yet to be released; we, however, expect them to perform better than segregated schemes, which recorded an average of 5.2% over one year, as they utilize their reserves to shore-up members’ returns and cushion their schemes from the poor performance in the equities markets experienced in 2018.

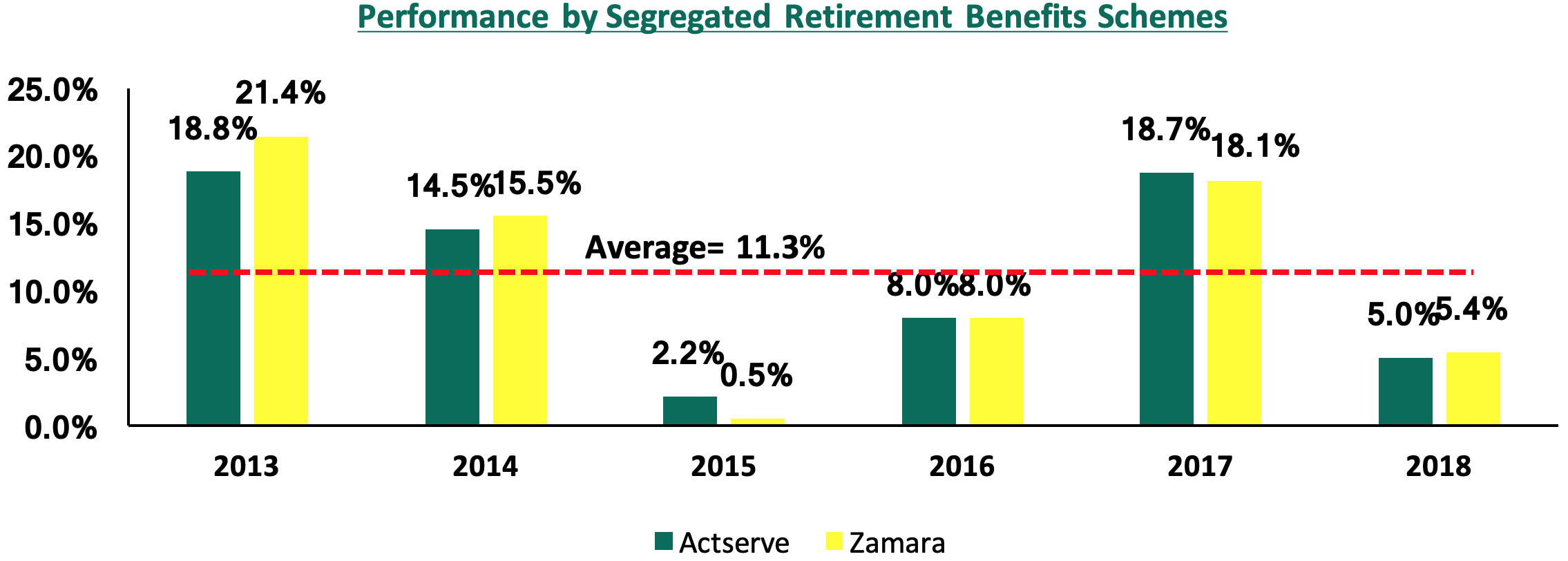

Segregated Schemes

Segregated Schemes are those where members’ contributions are invested directly by the Trustees via an appointed Fund Manager. The declared returns are based on what the fund achieves, fewer expenses, for the period in the review and the returns are fully accrued to the scheme for the benefit of members. In Kenya, there are two reports that are released on an annual basis. These are the Actuarial Services Company (EA) Limited (Actserve) Pension Schemes Investment Performance Survey, and the Zamara Consulting Actuaries Schemes Survey (Z-CASS).

For the year 2018, the Actserve and Z-CASS reports have indicated average returns for segregated schemes came in at 5.2% (Z-CASS reporting 5.4% and Actserve reporting 5.0%), a 71.7% decline (representing a decline of 13.2% points) from the 18.4% declared in 2017 (Z-CASS reporting 18.1% and Actserve reporting 18.7% in 2017).

The low performance was greatly attributed to the protracted bear run in the equities market in 2018, which wiped out about Kshs 488.0 bn of investors wealth in the bourse, with NASI and NSE 20 declining by 18.0%, and 23.7%, respectively, in contrast to 2017, where NASI and NSE 20 rose by 27.0% and 16.5%, respectively. Schemes that have huge exposures in the equities market reported much lower returns. The lackluster performance in the equities markets can be attributed to;

Section III. Conclusion and outlook

Given the continued changes in the Retirement Benefits Industry and increased knowledge of investments, the sector is expected to do well both in terms of growth and returns offered to members. This can be further supported through:

You cannot copy content of this page